Union Connect: Despite Turbulent Times: Opportunities in Selected Risk Assets

|

|

|

|

Despite the conflict in the Middle East, the global economy has so far proved resilient. Supply bottlenecks, particularly in oil and liquefied natural gas, are likely to have only a temporary dampening effect on growth prospects, especially in Europe. Nevertheless, selected asset classes continue to offer opportunities for investors.

Europe is currently feeling the effects of multiple geopolitical crises and elevated energy prices. Nevertheless, the economy has coped well with the energy supply shock. Much of the shortfall in oil from the Middle East has been offset by higher production in other countries and by drawing on inventories. This has limited the rise in crude oil prices. However, this solution cannot be sustained indefinitely. Under the current status quo, inventory levels could become critical during the summer months. Our expectation, however, is that a solution will be found for the closure of the Strait of Hormuz before supply becomes worryingly tight as inventories are depleted.

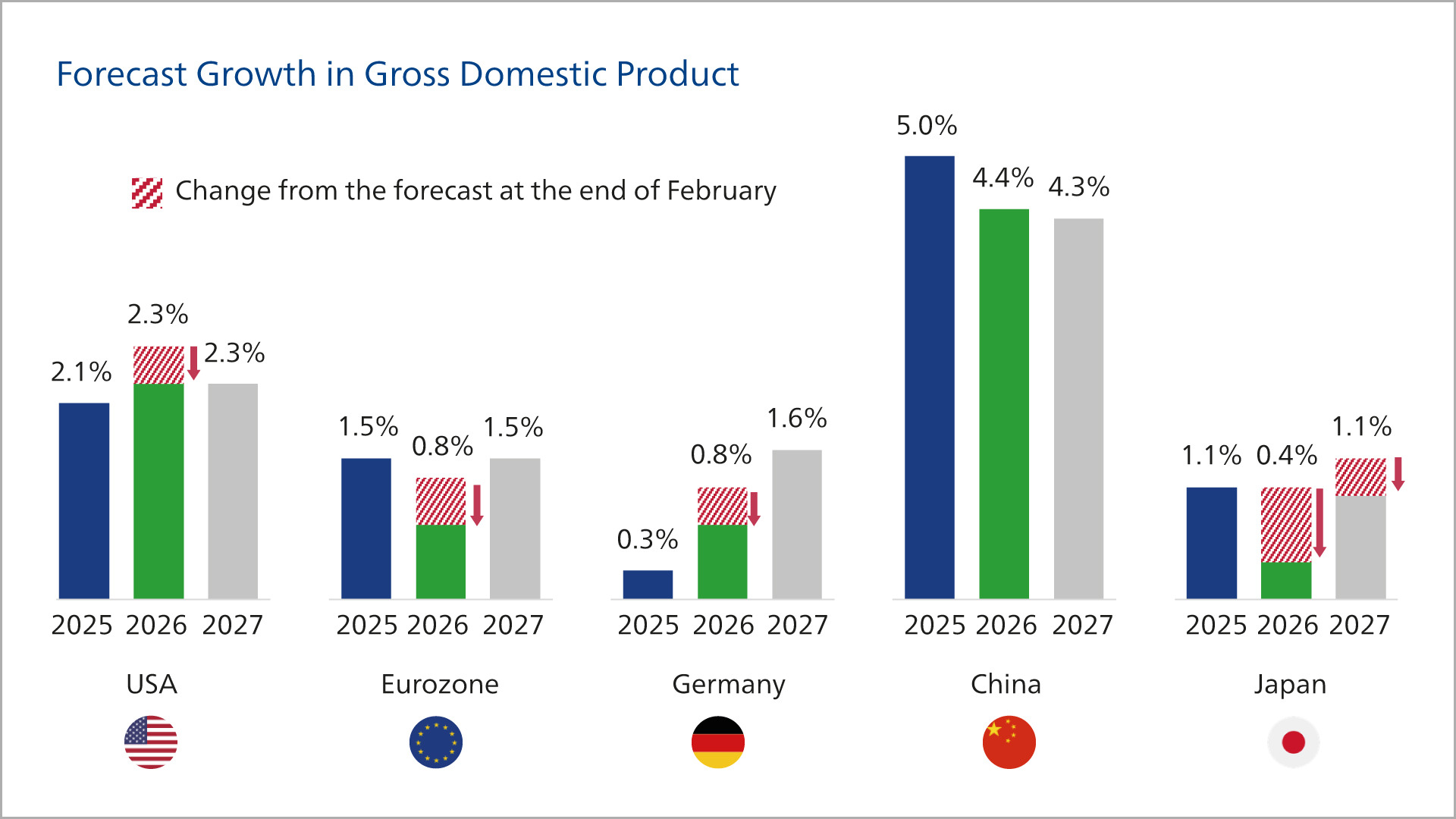

Iran Conflict Weighs on Growth in 2026

A prolonged closure of the Strait of Hormuz would further cloud the economic outlook

Source: Union Investment. As at 1 June 2026.

This should also help Germany avoid another year of zero growth. We do not expect the eurozone to slip into recession as a result of high energy prices. Overall, the German economy is likely to grow by 0.8 per cent for the year, matching the pace of the eurozone. For the United States, Union Investment's experts expect growth of 2.3 per cent, supported by the country's energy independence and driven by the megatrend of artificial intelligence (AI). However, if the Strait of Hormuz remains closed for an extended period, the economic consequences in the second half of the year would be severe. In such a scenario, the oil price could rise persistently and significantly above the threshold of US$120 per barrel, with equity markets also likely to come under pressure.

No Second-Round Effects in Europe

Monetary policy cannot directly counter a supply shock. Its role is to monitor potential second-round effects and longer-term inflation expectations. If these rise, central banks face a dilemma: on the one hand, they need to keep inflation expectations in check; on the other, they must avoid adding to the growth burden caused by the supply shock through further interest-rate hikes. The situation is particularly delicate for the European Central Bank (ECB), as its mandate is focused solely on price stability. We do not expect either Europe or the US to be on the brink of a new cycle of interest-rate increases. The current situation is not comparable to 2022, when persistent inflation led to substantial rate hikes.

As a hedge against higher inflation expectations, however, the ECB is likely to implement one or two interest-rate hikes in the near term. The US Federal Reserve, by contrast, is expected to adopt a slightly more expansionary stance towards the end of the year despite the rise in inflation. This is due to the new Fed Chair Kevin Warsh, who firmly believes in future productivity gains from artificial intelligence. Union Investment's experts expect the Fed to cut rates twice in the winter half-year of 2026/27.

In our view, the outcome of the US congressional midterm elections in November is unlikely to have much influence on the actions of US President Donald Trump. While the Democrats have a good chance of winning a majority in the House of Representatives and possibly even in the Senate, this is unlikely to fundamentally change the political dynamics in Washington. In recent months, the US President has repeatedly demonstrated how policy can be pursued by circumventing Congress.

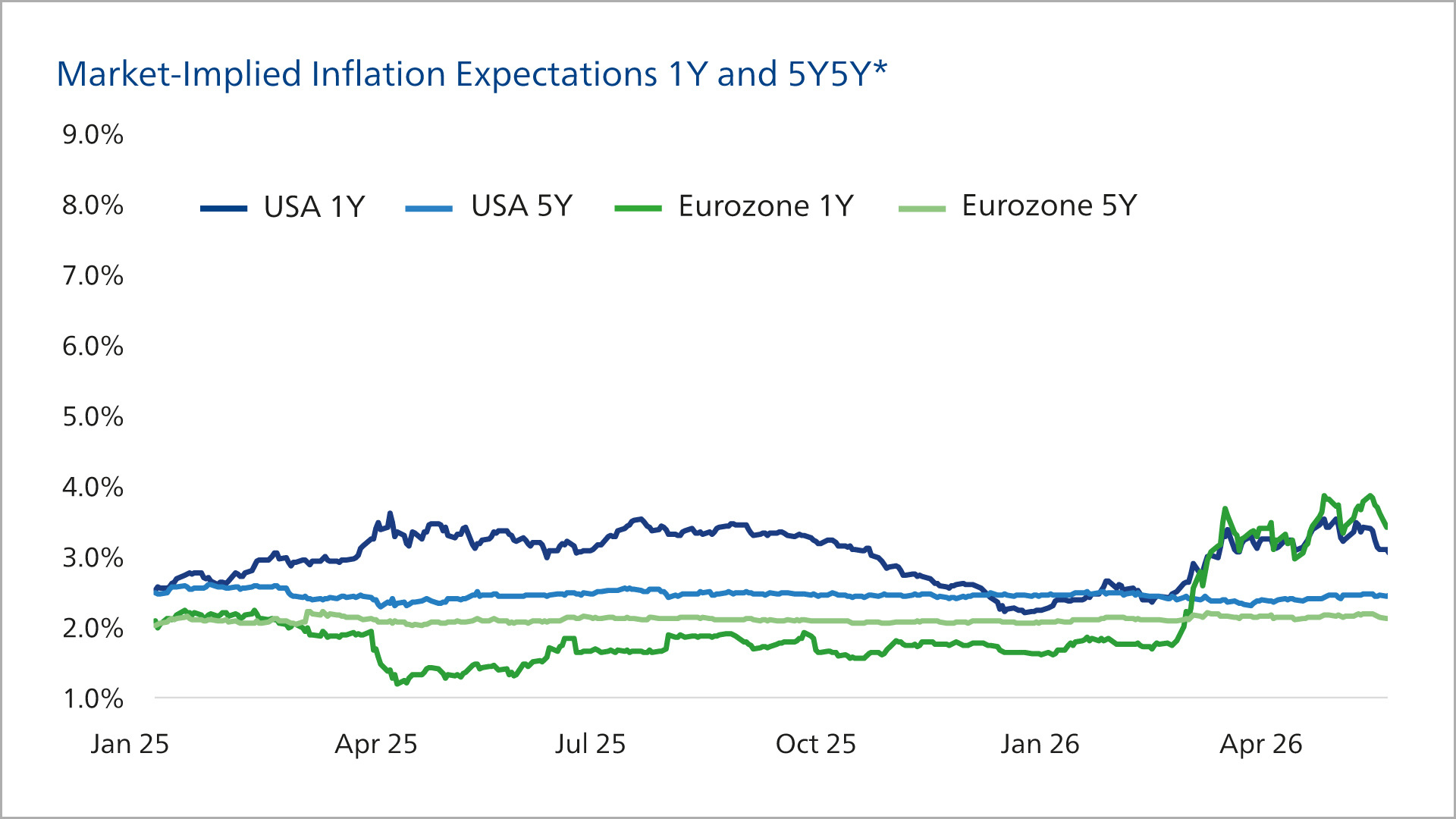

Short-Term Inflation Expectations Have Risen, While Longer-Term Expectations Remain Anchored

Short-term inflation expected to rise – but not over the long term

Source: Bloomberg, Union Investment. As at 31 May 2026. *Inflation swap zero coupon 1Y and inflation swaps forward 5Y5Y

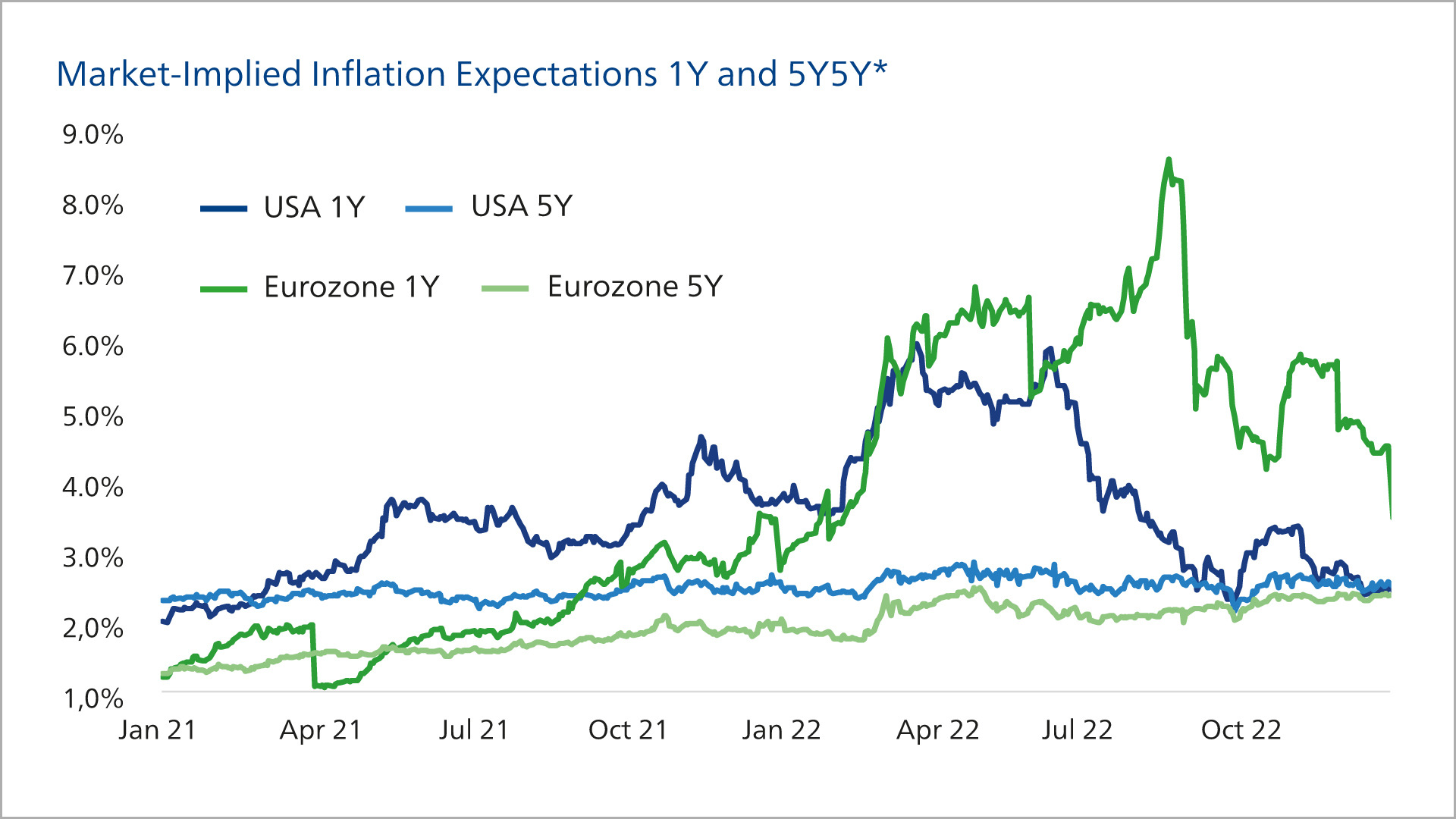

The inflationary impulse was much stronger in 2022

Source: Bloomberg, Union Investment. As at 31 May 2026. *Inflation swap zero coupon 1Y and 5Y5Y forward inflation swaps

As a hedge against higher inflation expectations, however, the ECB is likely to implement one or two interest-rate hikes in the near term. The US Federal Reserve, by contrast, is expected to adopt a slightly more expansionary stance towards the end of the year despite the rise in inflation. This is due to the new Fed Chair Kevin Warsh, who firmly believes in future productivity gains from artificial intelligence. Union Investment's experts expect the Fed to cut rates twice in the winter half-year of 2026/27.

In our view, the outcome of the US congressional midterm elections in November is unlikely to have much influence on the actions of US President Donald Trump. While the Democrats have a good chance of winning a majority in the House of Representatives and possibly even in the Senate, this is unlikely to fundamentally change the political dynamics in Washington. In recent months, the US President has repeatedly demonstrated how policy can be pursued by circumventing Congress.

AI Remains a Key Driver of Equity Markets

In global equity markets, artificial intelligence (AI) remains a key driver. Earnings growth is solid across a broad range of companies, but AI continues to dominate markets despite all geopolitical uncertainties. Major players such as Nvidia, Meta and Alphabet continue to invest on a large scale, irrespective of whether a barrel of oil costs US$80 or US$120. As a result, the US market currently remains particularly promising for investors.

However, it is important to differentiate between those technology companies that are genuinely benefiting from AI and those exposed to disruption risks. While the AI winners, for example in the semiconductor sector, are now trading at elevated valuation levels, these higher valuations are justified by their earnings and earnings prospects. The forthcoming IPOs of SpaceX and OpenAI are likely to provide an indication of whether investors remain willing to commit substantial amounts of capital to AI companies, or whether there are early signs of cooling. With a view to this megatrend, however, it may also be worthwhile to invest selectively in emerging markets. Asia in particular is home to many of the beneficiaries of the major AI-related investments.

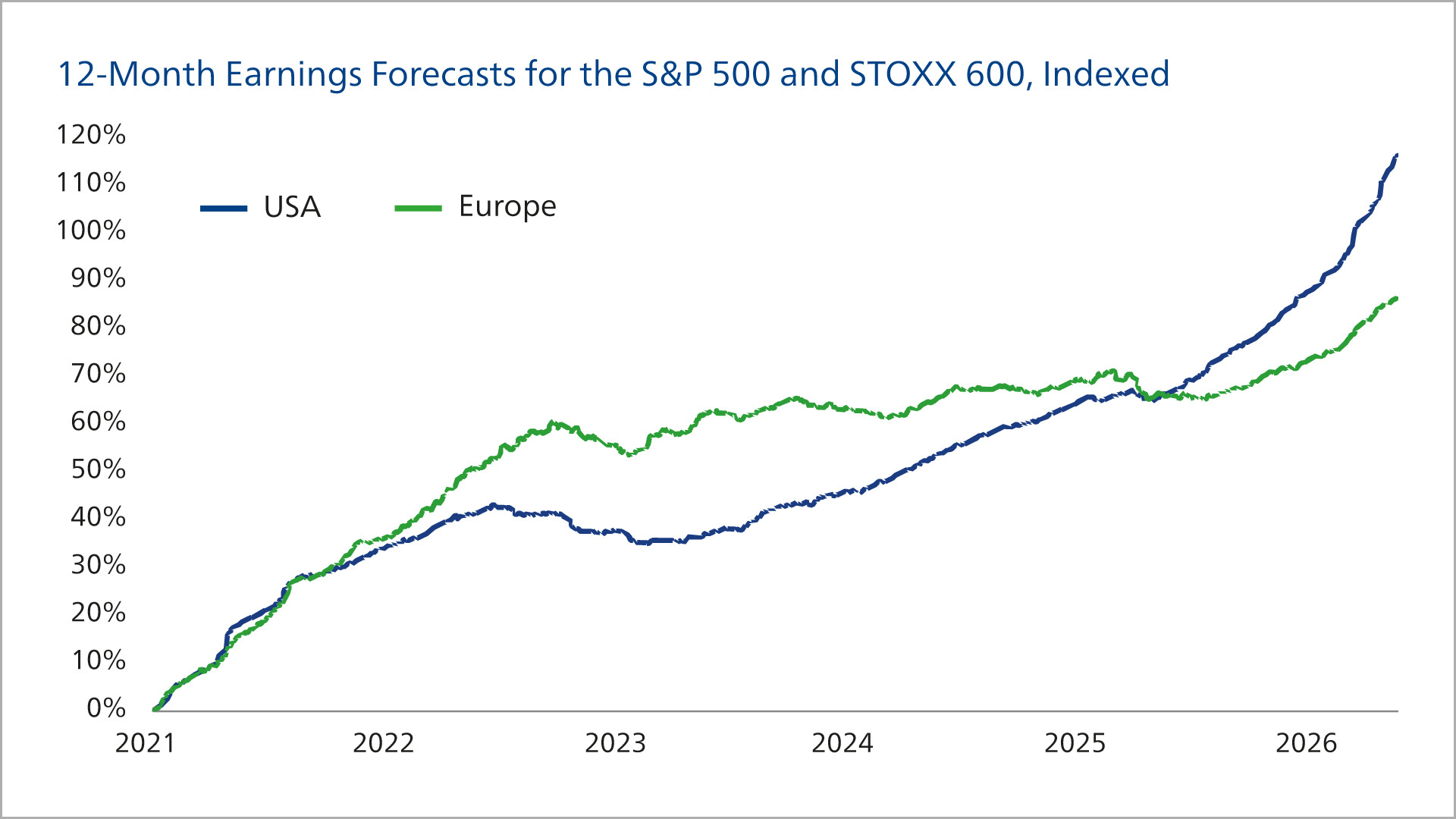

Earnings forecasts revised up further

In Europe, by contrast, markets are more likely to be weighed down by high energy prices – both through the earnings situation of individual companies and through the overall economic outlook. This makes a high degree of care in stock selection essential.

In principle, there is still much to be said for cyclical companies. Particular attention should be paid to names with a strong market position and pricing power. These companies are able to pass on higher costs to customers even in an environment of elevated inflation, thereby protecting their margins. Overall, however, the position of European companies remains robust, and earnings momentum is still intact despite the many geopolitical flashpoints. At the same time, we are seeing a wider valuation discount for European names compared with their US counterparts. This discount should narrow if the situation in the Middle East calms down again in the coming months and energy prices normalise.

However, it is important to differentiate between those technology companies that are genuinely benefiting from AI and those exposed to disruption risks. While the AI winners, for example in the semiconductor sector, are now trading at elevated valuation levels, these higher valuations are justified by their earnings and earnings prospects. The forthcoming IPOs of SpaceX and OpenAI are likely to provide an indication of whether investors remain willing to commit substantial amounts of capital to AI companies, or whether there are early signs of cooling. With a view to this megatrend, however, it may also be worthwhile to invest selectively in emerging markets. Asia in particular is home to many of the beneficiaries of the major AI-related investments.

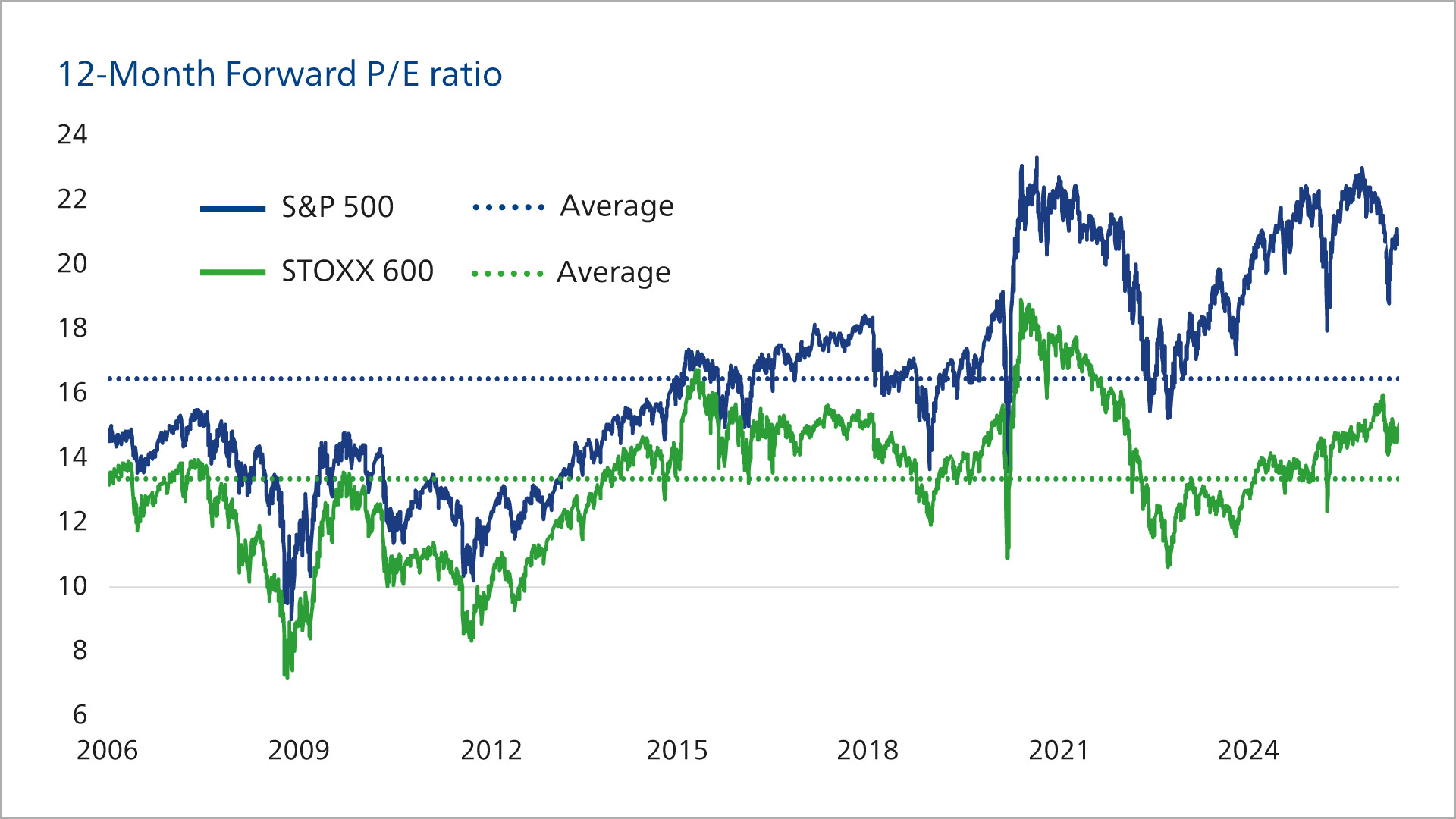

Corporate Earnings Are Accelerating Amid Elevated Valuations – Selection Remains Key

Earnings forecasts revised up further

Source: Bloomberg, Union Investment. As at 27 May 2026.

Valuations remain elevated despite the correction

Source: Bloomberg, Union Investment. As at 27 May 2026.

In Europe, by contrast, markets are more likely to be weighed down by high energy prices – both through the earnings situation of individual companies and through the overall economic outlook. This makes a high degree of care in stock selection essential.

In principle, there is still much to be said for cyclical companies. Particular attention should be paid to names with a strong market position and pricing power. These companies are able to pass on higher costs to customers even in an environment of elevated inflation, thereby protecting their margins. Overall, however, the position of European companies remains robust, and earnings momentum is still intact despite the many geopolitical flashpoints. At the same time, we are seeing a wider valuation discount for European names compared with their US counterparts. This discount should narrow if the situation in the Middle East calms down again in the coming months and energy prices normalise.

Corporate Bonds Remain Well Supported

At the bond markets, corporate bonds with good to very good credit quality (investment grade) remain well supported, although the decline in risk premiums means that their price potential is limited. For government bonds, rising net issuance volumes — driven by high levels of public investment and budget deficits — are creating headwinds. Another factor weighing on government bonds is the withdrawal of central banks as buyers, as the major purchase programmes are not being continued. In addition, there is a shift in credit quality from sovereigns to companies. Government debt is on an upward trend, while corporate debt remains stable.

In this environment, good-quality corporate bonds have taken on the role of government bonds for many investors. Corporate bonds have become a kind of new “safe haven”. Against the backdrop of steepening yield curves, bonds in the intermediate maturity segment look attractive. Long-dated government bonds in particular carry the risk that capital losses could erode the coupon. In terms of country allocation, we prefer the euro periphery over German government bonds, given the more positive rating momentum. By the end of the year, the yield on ten-year German Bunds is expected to stand at 3.25 per cent. US Treasuries with the same maturity are likely to yield 4.75 per cent.

In this environment, good-quality corporate bonds have taken on the role of government bonds for many investors. Corporate bonds have become a kind of new “safe haven”. Against the backdrop of steepening yield curves, bonds in the intermediate maturity segment look attractive. Long-dated government bonds in particular carry the risk that capital losses could erode the coupon. In terms of country allocation, we prefer the euro periphery over German government bonds, given the more positive rating momentum. By the end of the year, the yield on ten-year German Bunds is expected to stand at 3.25 per cent. US Treasuries with the same maturity are likely to yield 4.75 per cent.

Iran War Drives Energy Commodity Prices Higher

The war in the Middle East and the resulting closure of the Strait of Hormuz have led to a historic supply shortfall in oil and liquefied natural gas. The release of strategic reserves can only partially cushion the production cuts in the Gulf region. Even if the parties to the conflict reach a swift agreement, supply is likely to remain lower for several months due to damage to infrastructure and the only gradual resolution of logistical and production-related disruptions. Nevertheless, oil and liquefied natural gas are likely to become cheaper again once the situation in the Persian Gulf has calmed down. We expect the price of Brent crude to stand at US$85 per barrel by the end of the year. However, this is conditional on the Strait of Hormuz being navigable again from the summer months onwards.

For industrial metals, concerns about the economic outlook are moving into focus and are tending to put downward pressure on prices. In some cases, however, supply disruptions caused by the Middle East conflict are offsetting this trend, for example in copper and nickel, where producers depend on sulphuric acid from the region. Over the long term, the positive drivers predominate, supported by electrification and the energy transition. For precious metals, we see only limited further upside. Despite the correction in the first half of the year, the gold price remains at a very high level and is well above production costs. This could lead to an expansion of production capacity and falling prices.

For industrial metals, concerns about the economic outlook are moving into focus and are tending to put downward pressure on prices. In some cases, however, supply disruptions caused by the Middle East conflict are offsetting this trend, for example in copper and nickel, where producers depend on sulphuric acid from the region. Over the long term, the positive drivers predominate, supported by electrification and the energy transition. For precious metals, we see only limited further upside. Despite the correction in the first half of the year, the gold price remains at a very high level and is well above production costs. This could lead to an expansion of production capacity and falling prices.

Prudent Selection and Diversification Are Essential

Overall, the capital markets continue to offer more opportunities than risks. Markets adapt to risks, and they are currently absorbing the geopolitical crisis environment well. We can look back on three strong capital market years in succession and are already well into the fourth. However, investors should remain vigilant. Fundamental analysis and prudent selection have a particularly important role to play in the current tense market environment, which is characterised by a wide range of uncertainties. Investors who take a close look and manage risks consciously can still generate adequate returns despite the persistent geopolitical headwinds. Given the many uncertainty factors, however, it remains essential to diversify investments across multiple asset classes and regions in order to cushion potential setbacks.

Note: References to individual securities and companies are provided for illustrative purposes only and do not constitute a recommendation to buy or sell these securities. The companies mentioned are not necessarily held in Union Investment portfolios. Assessments may change, and the company concerned may already have responded to such changes.

Note: References to individual securities and companies are provided for illustrative purposes only and do not constitute a recommendation to buy or sell these securities. The companies mentioned are not necessarily held in Union Investment portfolios. Assessments may change, and the company concerned may already have responded to such changes.

Source: Union Investment, All information, explanations and representations are as at 9 June 2026, unless otherwise stated