Union Connect: Hard assets have potential again

|

|

|

|

The current crises present investors with a range of challenges: established correlations are being questioned, and rapid shifts in market direction demand adaptive behaviour. On the equity side, there are various ways to increase portfolio stability through diversification.

Mr Rautenberg, the current situation in the capital markets is volatile. The developments are quite dispersed both in terms of regional allocation and sector performance. How do you navigate equity portfolios through this environment?

Arne Rautenberg: The conflict in the Middle East and the resulting market turbulence demonstrate once again that when stress enters the system, investors tend to seek refuge in the US dollar. This reflex still holds true—despite all the scepticism about a structural weakness of the greenback. What applies to the US dollar also applies to US equities: they have clearly outperformed their European counterparts during the Iran conflict. Admittedly, the US is more energy independent than Europe. The S&P 500 index lost just under five percent in the critical month of March, whereas the European STOXX 600 index fell by almost eight percent. Since then, US equity indices have reached new highs, while on the old continent the level of February this year has not yet been surpassed.

So, does the war in the Middle East have less of a significant impact on the equity markets than initially expected?

Arne Rautenberg: What has changed as a result is the economic momentum in different regions of the world. Until the end of February, market participants still assumed that tax rebates in the US would support consumption and that large investment programmes in Europe would lead to increased demand and thus more growth. This thesis remains valid, but investors looking to invest in cyclical companies should consider an additional factor. Due to higher energy prices as a consequence of the war, increased inflation is to be expected. Cyclical companies therefore face the risk of margin erosion during growth phases. That is why pricing power is currently a decisive factor in stock selection. A company that is strongly positioned in the competitive landscape or even has a unique selling point is better able to pass on price increases to its customers. This helps protect its own profit and loss account. History shows that such companies can even expand their margins during periods of rising inflation—as we are currently seeing.

During the first-quarter earnings season, the major US tech names once again stood out with significant revenue growth. How long is this trend expected to continue?

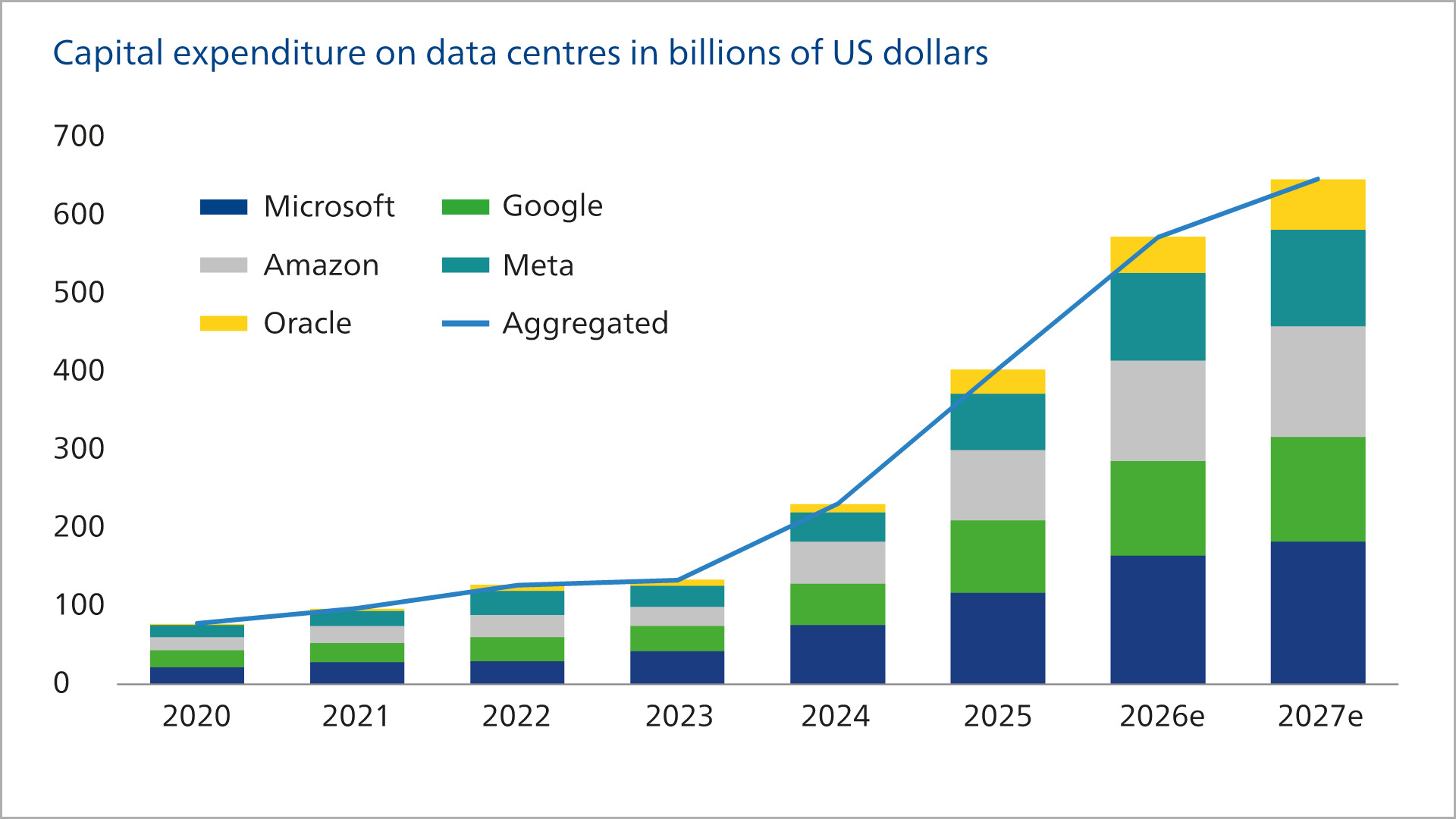

Arne Rautenberg: Currently, we observe that the major players in the field of artificial intelligence (AI) are investing enormous resources in capacity expansion. Companies such as Alphabet or Meta are hardly concerned whether the price of a barrel of oil is 80 or 120 US dollars, or whether US politics is erratic or not.

Continued increasing AI investments by major US market players

Acceleration in the investment supercycle

Source: Bloomberg, Union Investment. As of 31 March 2026. * All figures are net return variants. Observation period from 1 April 2021 to 31 March 2026, each in one-year intervals. Performance data are based on past values and do not provide reliable indications of future performance.

Arne Rautenberg: The AI trend is somewhat independent of the crises affecting the world and therefore remains a long-term, significant growth driver for the equity market as well as the overall economy. Increasingly, companies across the industrial sector are deploying AI to boost their productivity. This broadens the AI trend. Relevant names, for example in the semiconductor sector or among platform operators, should therefore be considered in portfolio construction. In terms of regional allocation, besides the US, some Asian economies such as Taiwan and South Korea are also worth a look. These countries produce high-quality components for AI data centres and applications. The AI trend has more focal points than just the US.

Beyond the AI theme, are there other essential factors for investors aiming to build a resilient equity portfolio?

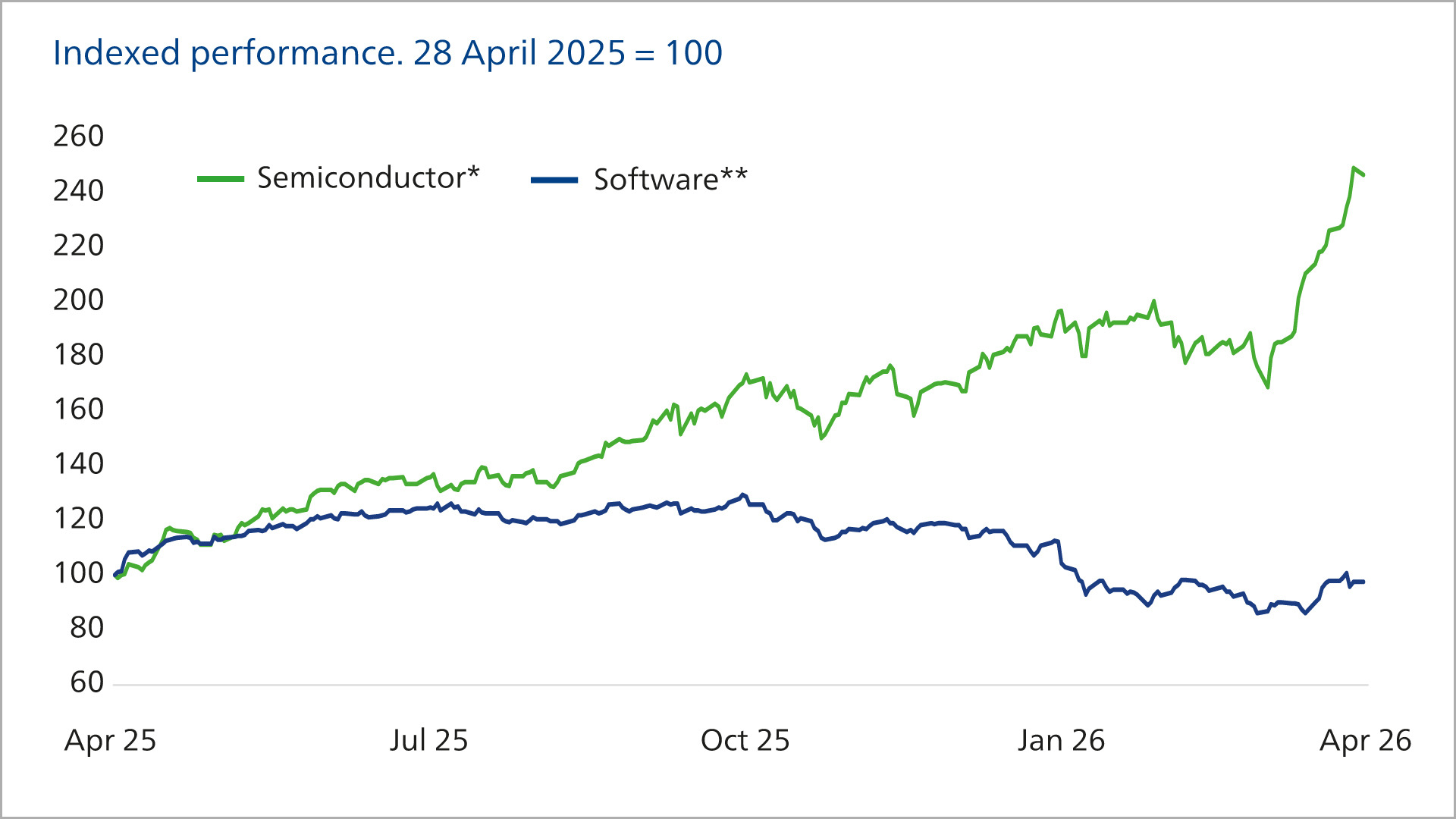

Arne Rautenberg: Yes. Business models with hard assets—that is, tangible balance sheet assets—are regaining potential. This applies, for example, to manufacturing companies in the so-called Old Economy. With the advent and spread of AI, many business models are being questioned and may become obsolete in the medium to long term. Sectors we refer to as "soft assets," which typically provide standard services in the service sector with relatively low capital intensity, are particularly negatively affected. Examples include call centres, payment and data service providers, as well as software product developers.

AI is transforming industries and companies

Disruption: Semiconductors Boom, Software Falters

Source: Bloomberg, Union Investment. As of 27 April 2026. * Philadelphia Semiconductor Sector, ** S&P 500 Software & Services.

So, is the "Old Economy" making a comeback in portfolios?

Arne Rautenberg: We believe that a higher allocation to hard assets does indeed make sense, but with due caution. The business models of the Old Economy are viable if these companies can demonstrate that they can use AI beneficially for themselves and their customers. This requires patience and does not exempt investors from conducting thorough individual stock analysis. After all, not all these companies are in excellent shape—some, however, certainly are. In the current phase of high energy costs, these can be companies that support governments in their quest for greater energy autonomy. Wind farm operators, renewable energy utilities, battery manufacturers, and insulation producers can, for example, be part of a resilient portfolio. At the same time, it can make sense in the short term to maintain positions in fossil fuel sectors. They have benefited from the closure of the Strait of Hormuz and will continue to do so as long as the situation remains uncertain.

Where do the European equity markets stand in this complex environment? The hope for a recovery in Europe was considerable; however, the price performance has yet to reflect this.

Arne Rautenberg: That is correct; however, we still see the potential. Notably, when focusing on hard assets, there is a regional shift towards Europe. In recent years, we have witnessed many new business models emerging from the US that have spread globally. Today, it is apparent that many of these originate from sectors now at risk of being displaced by AI. While the German and European economies can be criticised for a certain sluggishness and cautious approach to innovation, this may actually turn into an advantage. The industry, which largely shapes the DAX, predominantly consists of hard assets. Thus, different drivers influence European markets compared to US equities. This presents significant diversification potential, as demonstrated during last year's "deep-sea shock." At that time, European equities outperformed US stocks for a period, due to the high market concentration and heavy reliance on technology stocks in the US, which came under pressure. While the top ten largest US stocks are 80 percent from the extended IT sector, Europe's top ten include five different industries. This diversity has become an advantage, alongside the comparatively more attractive valuation on the Old Continent. The average price-to-earnings ratio for US stocks currently stands at 20 based on expected earnings for the coming year, whereas in Europe it is only 15. Last but not least, from a euro perspective, investing in European equities offers the benefit of diversifying the portfolio away from the US dollar to some extent — a prudent approach given the long-term challenges associated with US debt developments.

|

40

Market concentration in the S&P 500 has increased significantly in recent years. The ten largest companies in the S&P 500 now account for approximately 40 percent of the entire index. In comparison, the European equity market is considerably more broadly diversified, with the top ten names representing only about one-fifth of the index’s total market capitalisation.

|

What role does geopolitics play for European stock markets?

Arne Rautenberg: The numerous crises act as a catalyst and should lead to higher valuations for European companies. Since Donald Trump took office in the White House, it has become clear that the transatlantic partnership is weakening. Europe must become more independent and has initiated the financing of measures to modernise and strengthen its autonomy through fiscal stimulus. This concerns the energy sector as well as defence and supply chains. Government spending also benefits domestic companies and potentially increases profits in the longer term. Although the war in the Middle East has delayed this development, it has underscored the urgency of the task impressively.

Source: Union Investment, All information, explanations and representations are as at 19 May 2026, unless otherwise stated