Union Connect: Central banks: No New Cycle of Interest Rate Hikes in Sight

|

|

|

|

The Iran conflict has stoked concerns about persistently higher energy prices and rising inflation. However, the situation is not comparable to the supply chain chaos following the COVID-19 pandemic. What impact will the Iran crisis have on monetary policy? Michael Herzum, Head of Economics & Macro Strategy, provides an assessment of the current situation.

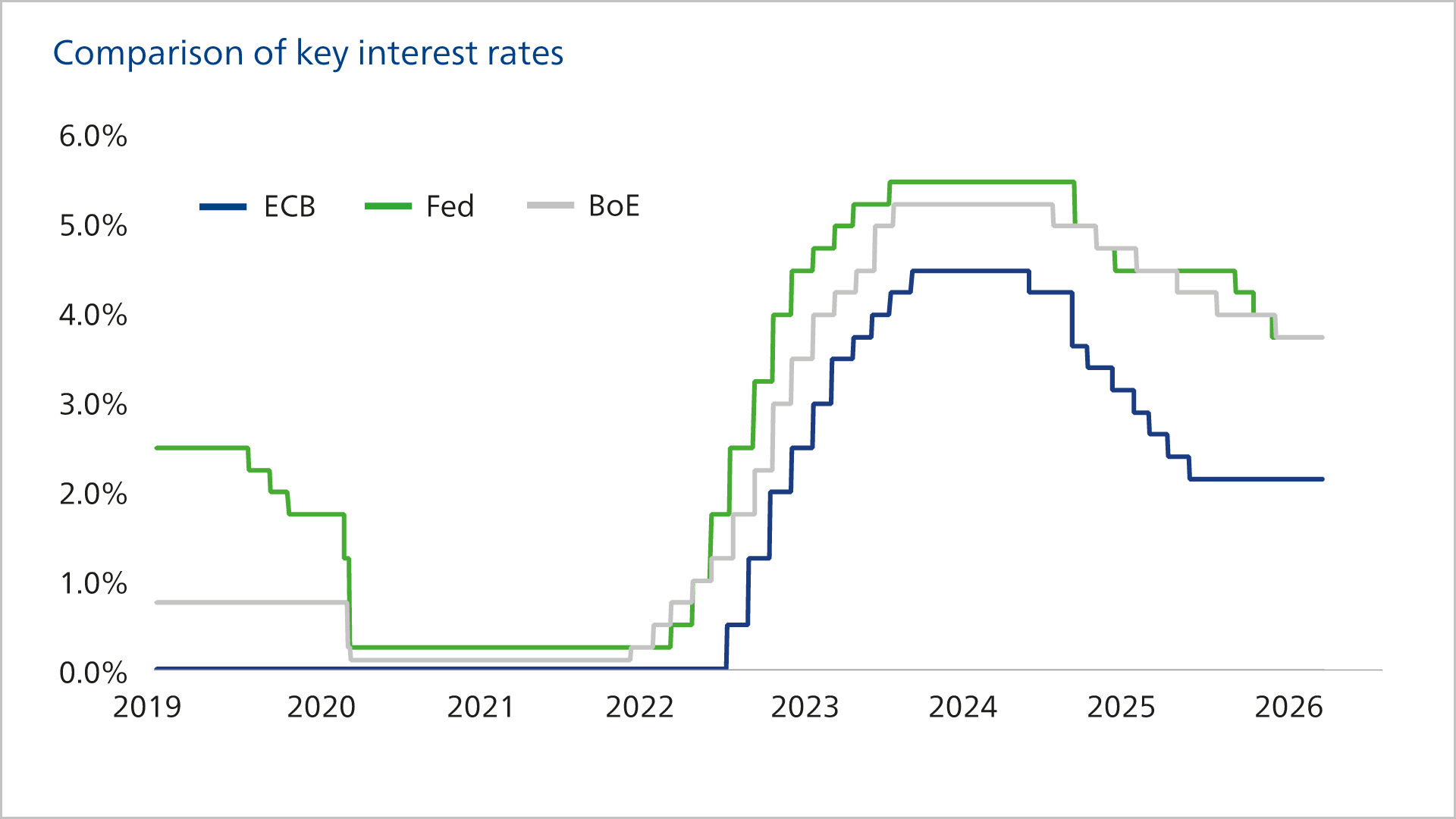

Investor concerns are high that energy prices will remain elevated over a prolonged period due to the Iran conflict. Some market participants fear that central banks might now initiate a cycle of interest rate hikes—comparable to that of 2022 and 2023. At that time, for instance, the ECB raised its deposit rate in ten steps from -0.5 percent to four percent. How quickly the Strait of Hormuz—crucial for the export of oil, gas, and petrochemical products—becomes freely navigable again will largely determine the macroeconomic impact of the crisis. The longer supply chains are disrupted and production facilities damaged, the greater the cumulative supply shortfall will be for crude oil, diesel, and kerosene, as well as for raw materials such as helium or fertilisers. Physical markets, especially in Asia but also in Europe, are beginning to show shortages that result in price increases and push inflation upward.

Impact on Inflation Not Comparable to Supply Chain Chaos After the Pandemic

From an investor’s perspective, it is crucial to understand the differences between today’s situation and that following the COVID-19 pandemic. The impact of the Iran crisis on inflation and monetary policy is likely to be far less pronounced than around five years ago, when a combination of factors drove inflation to levels reminiscent of the 1970s. This then forced central banks to implement sharp interest rate hikes. At that time, numerous industrial supply chains worldwide were disrupted due to the pandemic. Essential goods such as semiconductors were in short supply, hampering the automotive industry. During lockdowns, households spent less on services like cinema or restaurant visits, shifting consumption towards goods, which overloaded goods production, especially in Asia. Even when goods could be produced, bottlenecks often occurred at ports or with shipping. In addition to supply chain problems, there was a demand shock. When anti-COVID measures eased, pent-up demand surged. Furthermore, a large fiscal stimulus by the US government under President Joe Biden overheated the economy in many areas, leading to second-round effects on inflation. With the onset of the Ukraine war in spring 2022, critical raw material deliveries—including natural gas—also ceased, further intensifying inflationary pressure.

This time it is a pure supply shock, mainly affecting largely interchangeable commodities that can be sourced elsewhere on the global market—albeit at higher prices. The overall economic environment is also different: the crisis hits the economy during a period of stable development, which in Europe is supported by government investments in defence and infrastructure. Unlike before, there has been no demand shock, and the economy is at risk of overheating due to pent-up demand and fiscal stimulus. Moreover, as interest rates are already at a level that is more or less neutral—not expansionary and growth-supporting—the starting point for central banks is different from early 2022, when low interest rates prevailed.

This time it is a pure supply shock, mainly affecting largely interchangeable commodities that can be sourced elsewhere on the global market—albeit at higher prices. The overall economic environment is also different: the crisis hits the economy during a period of stable development, which in Europe is supported by government investments in defence and infrastructure. Unlike before, there has been no demand shock, and the economy is at risk of overheating due to pent-up demand and fiscal stimulus. Moreover, as interest rates are already at a level that is more or less neutral—not expansionary and growth-supporting—the starting point for central banks is different from early 2022, when low interest rates prevailed.

Inflation Concerns Increase Pressure on Central Banks to Act

US interest rate cuts fully priced in

Source: Bloomberg, as of 17 April 2026

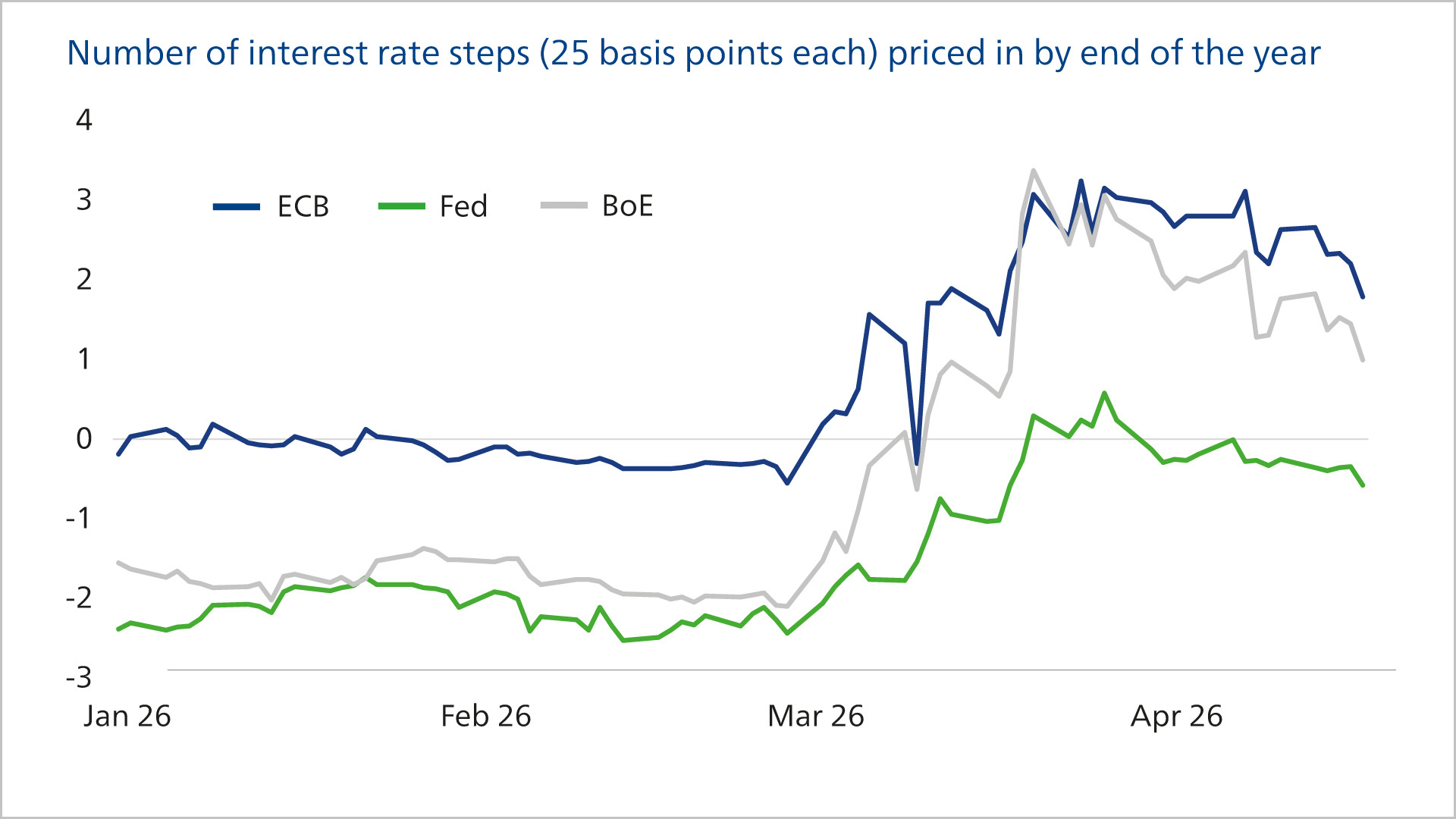

Key interest rate expectations adjust significantly upwards

Source: Bloomberg, as of 17 April 2026

|

The Iran war and the resulting sharp rise in energy prices have led capital markets to expect ECB interest rate hikes. At the end of March, based on futures contracts, the financial market priced in three ECB rate hikes by the end of this year. Meanwhile, this has been revised down to two hikes - still "too many," according to our experts in their baseline scenario.

|

Monetary Policy Can Do Little in the Face of a Supply Shock

Although the situation remains fragile and a final resolution of the Iran conflict is likely only after lengthy and difficult negotiations, we assume that neither the US nor Iran has an interest in renewed military escalation. The currently high gasoline and diesel prices in the US are "poison" for Donald Trump's Republicans six months before the midterm elections in November. Moreover, the militarily and economically significantly weakened Iran cannot afford to go without its oil revenues for long. Our baseline scenario therefore assumes a gradual easing of the situation and falling energy prices towards the end of the year. The inflation rise in the second quarter is now clear but likely of limited duration.

Monetary policy cannot directly counter the supply shock. Its task is to keep an eye on long-term inflation expectations. If these rise, central banks face a dilemma. On the one hand, they must keep inflation expectations in check; on the other hand, they must not further burden growth with interest rate hikes given the supply shock in energy markets. The situation is a tightrope walk, especially for the European Central Bank (ECB), as its mandate is solely focused on price stability. We believe both the ECB and the Fed can look through the Iran crisis as long as there are no second-round effects or entrenched inflation expectations.

Crucial for us, if the conflict continues with a sustained disruption of the Strait of Hormuz, will be data on prices and inflation expectations. In the case of a prolonged war (until the ECB meeting on 30 April and foreseeably beyond), individual rate hikes as currently priced by the market (two steps by year-end) cannot be ruled out. However, we consider the start of a new ECB rate hike cycle unlikely.

Monetary policy cannot directly counter the supply shock. Its task is to keep an eye on long-term inflation expectations. If these rise, central banks face a dilemma. On the one hand, they must keep inflation expectations in check; on the other hand, they must not further burden growth with interest rate hikes given the supply shock in energy markets. The situation is a tightrope walk, especially for the European Central Bank (ECB), as its mandate is solely focused on price stability. We believe both the ECB and the Fed can look through the Iran crisis as long as there are no second-round effects or entrenched inflation expectations.

Crucial for us, if the conflict continues with a sustained disruption of the Strait of Hormuz, will be data on prices and inflation expectations. In the case of a prolonged war (until the ECB meeting on 30 April and foreseeably beyond), individual rate hikes as currently priced by the market (two steps by year-end) cannot be ruled out. However, we consider the start of a new ECB rate hike cycle unlikely.

More Significant Consequences Will Only Arise in the Event of a Prolonged War

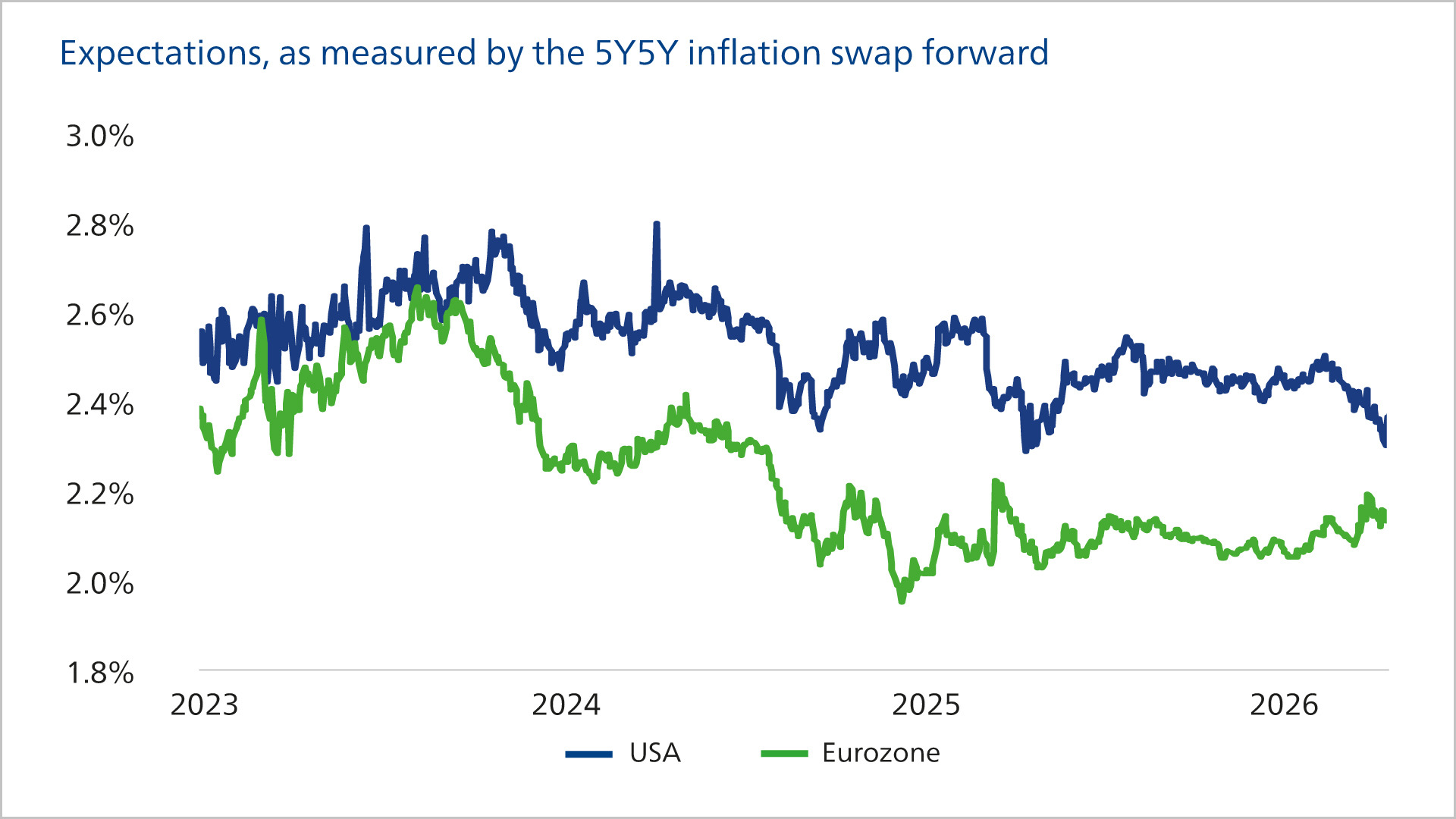

US inflation expectations are declining

Source: Bloomberg, as of 17 April 2026

Fed Likely to Cut Rates, BoJ Expected to Raise them.

The US Federal Reserve is expected to see a leadership change soon, with Kevin Warsh likely to replace Jerome Powell, although final confirmation is pending. Under Warsh, interest rate cuts are more likely, even if we view them as fundamentally unjustified.

We expect further interest rate hikes from the Bank of Japan (BoJ), starting from a different position. Compared to other central banks, the BoJ is "behind the curve" in monetary policy, having only begun raising rates late in 2024. Despite Japan's high dependence on energy imports and related inflation risks, the macroeconomic environment is solid. In light of the more expansionary fiscal policy under newly elected Prime Minister Sanae Takaichi, we anticipate two rate hikes in 2026 and three more in the following year. Depending on energy price developments, the BoJ might be forced to implement even more drastic rate increases. Overall, our view remains unchanged: we expect the impact of the Middle East conflict on energy markets to ease soon, supporting a largely stable economic outlook.

We expect further interest rate hikes from the Bank of Japan (BoJ), starting from a different position. Compared to other central banks, the BoJ is "behind the curve" in monetary policy, having only begun raising rates late in 2024. Despite Japan's high dependence on energy imports and related inflation risks, the macroeconomic environment is solid. In light of the more expansionary fiscal policy under newly elected Prime Minister Sanae Takaichi, we anticipate two rate hikes in 2026 and three more in the following year. Depending on energy price developments, the BoJ might be forced to implement even more drastic rate increases. Overall, our view remains unchanged: we expect the impact of the Middle East conflict on energy markets to ease soon, supporting a largely stable economic outlook.

Source: Union Investment, All information, explanations and illustrations are as at 20 April 2026, unless otherwise stated