Union Connect: Perspectives for the bond market 2026

|

|

|

|

This article was originally prepared for European Investors and may reflect a euro-based perspective. Investors with assets not denominated in their home currency are exposed to currency risk, which may affect the performance of the investment due to movements in the exchange rate between the asset's currency and the investor's home currency.

The US dollar is the most important global reserve currency, but now the race is being reopened. The euro has a chance to gain global significance – European bond investors would benefit from this. However, a success story is tied to concrete changes.The market environment for 2026 promises somewhat higher growth dynamics, alongside diverging interest rate and inflation developments between the USA and the Eurozone. This is likely to be reflected in a good performance of investment-grade corporate bonds in the bond markets. Caution is advised with government bonds, explains Christian Kopf.

Christian, we look back on a good year in the bond markets. What do you expect from 2026? Will the trend continue?

Christian Kopf: As far as corporate bonds are concerned, I am actually very optimistic. The risks for investment-grade securities are currently limited. Our statement that creditworthy corporate bonds have become a kind of new 'safe haven' for bond investors still holds true. We recommend euro-denominated bonds, as no currency hedging is necessary here. For losses to occur for a new investor over a one-year horizon at the current level, an interest rate increase of at least 25 basis points and a doubling of risk premiums would be required. We consider that unlikely.

From an interest rate perspective, the picture may fit, as we do not expect any interest rate hikes from the European Central Bank in 2026 due to the loose US Federal Reserve. Why are you so relaxed regarding the risk premiums?

Christian Kopf: I see two factors here. On the one hand, there is a higher economic dynamism that is likely to arise in Europe due to the implementation of fiscal packages. Especially in the USA, but also in Germany, there is a political willingness to increase debt in order to stimulate the economy. This is a break from the past and should manifest in a higher willingness to invest and, consequently, in rising corporate profits in the medium term. It is important for me to emphasize that companies, unlike states, can adapt more quickly to changes. On the other hand, the balance sheet quality of companies in the investment-grade sector is overall so good that even an unexpected economic downturn would have little impact on creditworthiness and credit profiles. All in all, we are in an environment where the yields on corporate bonds should be well captured.

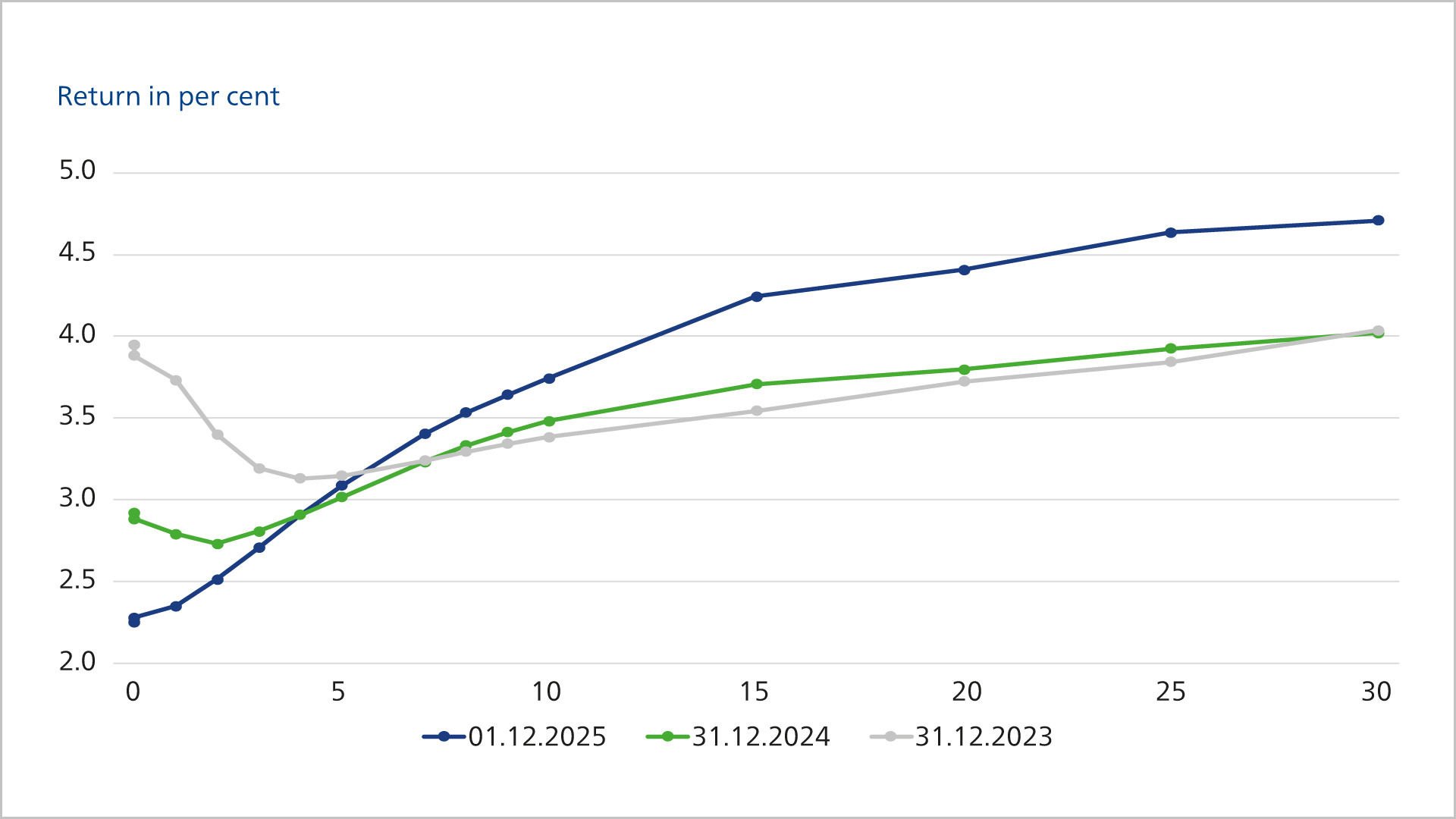

Investors not only look at the spread level but also at the curve steepness and thus at the yield perspective.

Investment-Grade Corporate Bonds EUR

Source: Bloomberg, Union Investment; Status: December 1, 2025.

You have mentioned the rising national debt. What can be expected for the bond markets as a result? Do you see any risks here?

Christian Kopf: Looking at the USA, I see that, yes. Washington's fiscal policy is not sustainable in the long run, which suggests further rising yields in the longer maturity area. However, this does not imply a systemic crisis; rather, it is an expression of a changed supply and demand situation. It is also contributed to by the fact that support from central bank purchases – known as quantitative easing – has fallen away. As a result, a potentially large buyer in the market is gone, while simultaneously the supply is increasing – in the end, private investors will have to buy more government bonds to absorb the new issuances. This will only be possible with higher yields. This will primarily affect the longer end of the yield curve, as long-term fiscal risks are rising due to the debt dynamics.

The market has so far viewed the issue of debt quite calmly. Why should investors remain vigilant?

Christian Kopf: As an institutional investor in the bond market, I believe one needs a certain degree of paranoia, meaning a focus on the tail risks. I don't want to paint a doomsday scenario, but when I consider what could happen in the coming year, I see a certain risk that an auction of US Treasuries could go awry, meaning that the supply is not fully placed with investors. This could lead to short-term fluctuations in the global bond markets, as Japan and some European countries have high levels of debt, and analogies could be drawn. However, this is likely to be only a temporary phenomenon. For the Federal Republic as an issuer, I do not see any substantial risks; the rating quality is not undermined by the increasing debt issuance. However, we expect a continued weakness of the US dollar. The reason for this is the political pressure on the US Federal Reserve to lower interest rates, which is likely to lead to a shrinking interest rate differential between the US and the Eurozone. An investor from the Eurozone can, if possible, remain in euros or hedge their US dollar positions.

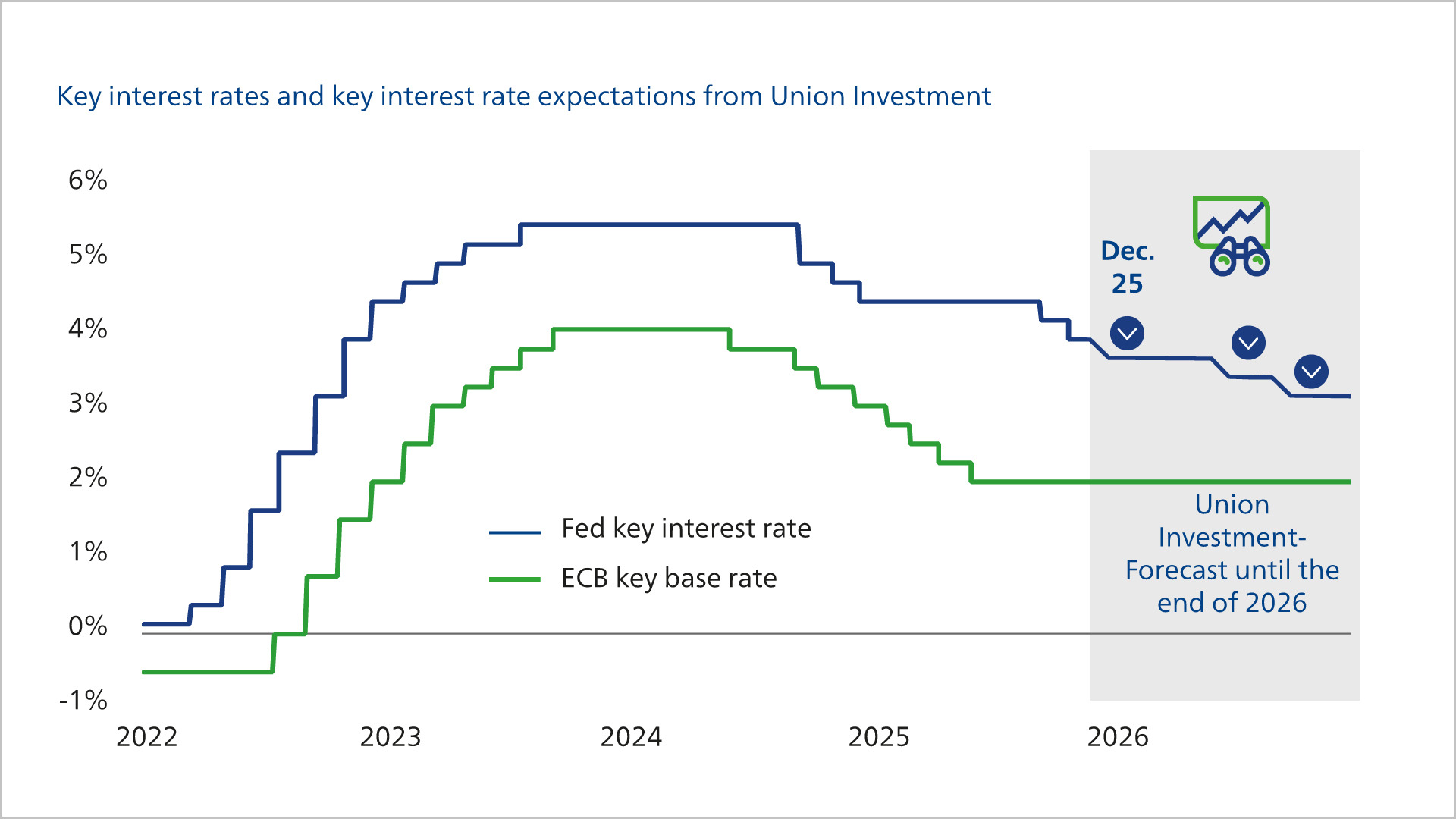

No change in monetary policy for fundamental reasons – Fed likely to cut due to political pressure.

We expect two interest rate cuts from the Fed in 2026.

Source: Macrobond, Union Investment. As of December 5, 2025.

Since US interest rates are likely to decline, the yield curve should steepen. Is there a theoretical upper limit to the yield difference between short-term and long-term bonds?

Christian Kopf: Yes, that is due to the roll yield. For example, if I buy a ten-year bond and hold it for a year, the yield decreases with a steep yield curve, and as a result, the price increases. If the curve is so steep that, thanks to a high roll yield, it is actually hardly possible to lose more money over a few months, regardless of how interest rates develop, then the maximum degree of steepness of the curve is likely to have been reached. However, in our opinion, this point has not yet been reached. Therefore, we recommend that investors initially avoid longer maturities in the government bond segment and keep the duration relatively short to limit loss risks.

The yield curves are likely to remain steep for a longer time?

Christian Kopf: Yes, due to the strong emission activity of the states and also because of the gradual erosion of the independence of the US Federal Reserve. Although inflationary pressure in the US will remain higher than in the Eurozone, partly due to the tariff policy of US President Trump, the US key interest rate is expected to decrease for political reasons. We anticipate two more rate cuts in 2026. Capital markets will have to adjust to fundamentally too low US key interest rates, which will support risk assets in the short term but pose new risks in the long term. While the short end of the yield curve is determined by the key interest rates, the risks of such a policy – possibly excessive inflation and increasing concerns about the refinancing ability of the US as an issuer – are likely to push yields higher in the longer maturities. In the Eurozone, there is another factor at play: the pension reform in the Netherlands, which suddenly turns pension funds into real asset managers, rather than primarily liability investors. Since the amount of pension commitments is no longer defined upfront, there is no target payout sum that needs to be achieved, allowing pension funds to invest more opportunistically and likely in areas that promise higher returns than government bonds.

|

4.75%

The ten-year US Treasury yield is expected to rise to 4.75 percent by the end of 2026, according to experts from Union Investment. After all, the ongoing interest rate should be able to more or less offset the expected price loss. In Japan, yields are also likely to rise due to persistently high inflation. Japanese investors hold the majority of Japanese government bonds, but they are sitting on significant book losses in their bond portfolios and therefore have little capacity to invest – even in US securities. Additionally, the attractiveness of Japanese securities increases with rising yields while US interest rates are falling. In the Eurozone, yields are also expected to rise for longer maturities: ten-year government bonds should trend upwards from the current level.

|

Good keyword – what can be expected in other fixed income segments in 2026, especially regarding carry products?

Christian Kopf: I had already pointed out that investment-grade corporate bonds in euros remain interesting. However, there are also other carry products such as covered bonds, securitizations—in the form of collateralized loan obligations (CLOs)—or selected emerging market securities in local currency that are promising. In particular, emerging market bonds benefit from falling US interest rates. At the same time, inflation in emerging markets is declining due to the increased import of cheap goods from China. We remain cautious towards government bonds from countries where high political instability meets high debt, such as France.

The new safe haven: The attractiveness of corporate bonds and covered bonds relative to government bonds is increasing.

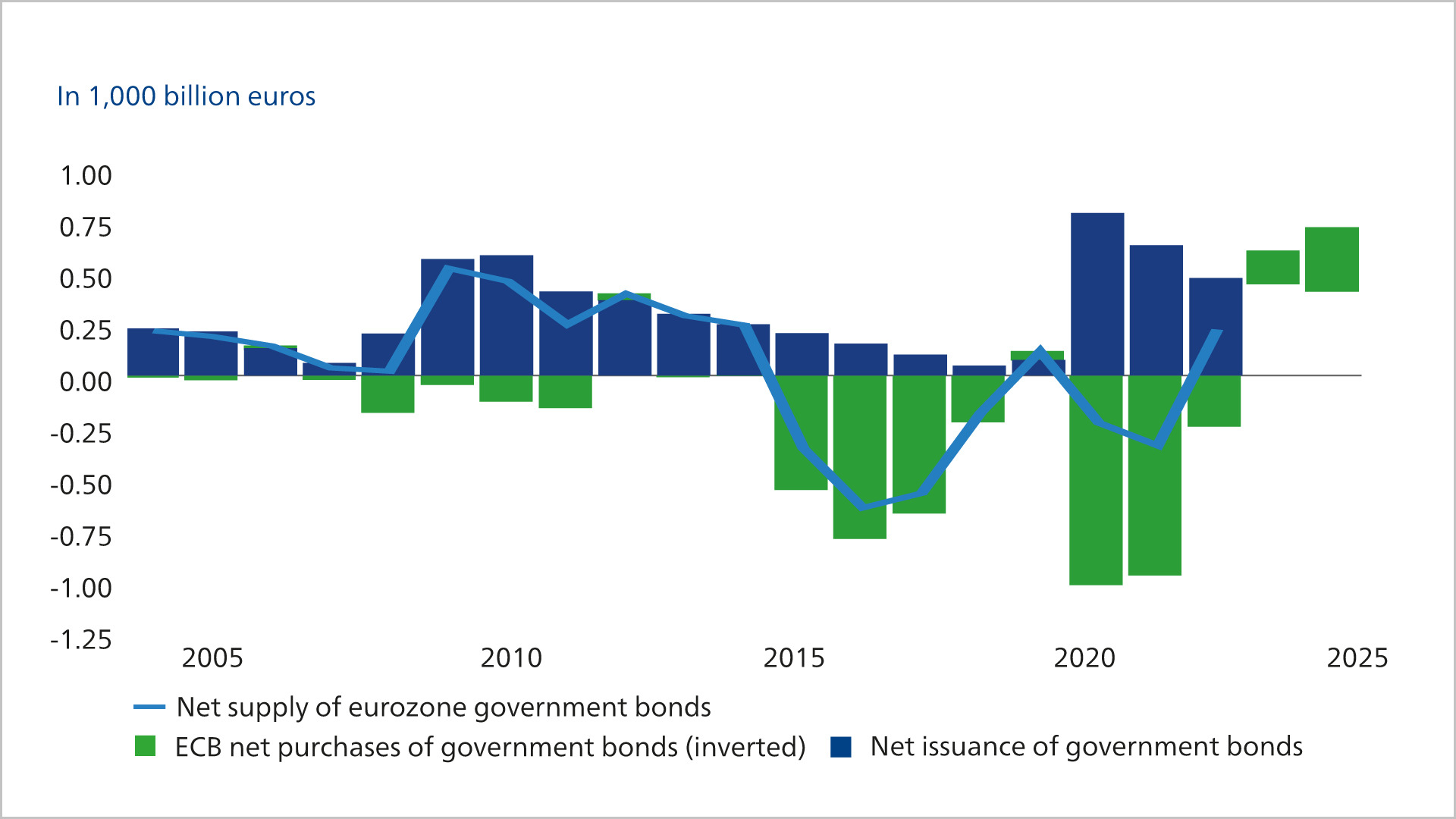

The ECB is no longer a buyer.

Source: ICE Indices, Macrobond, Union Investment. As of: December 1, 2025

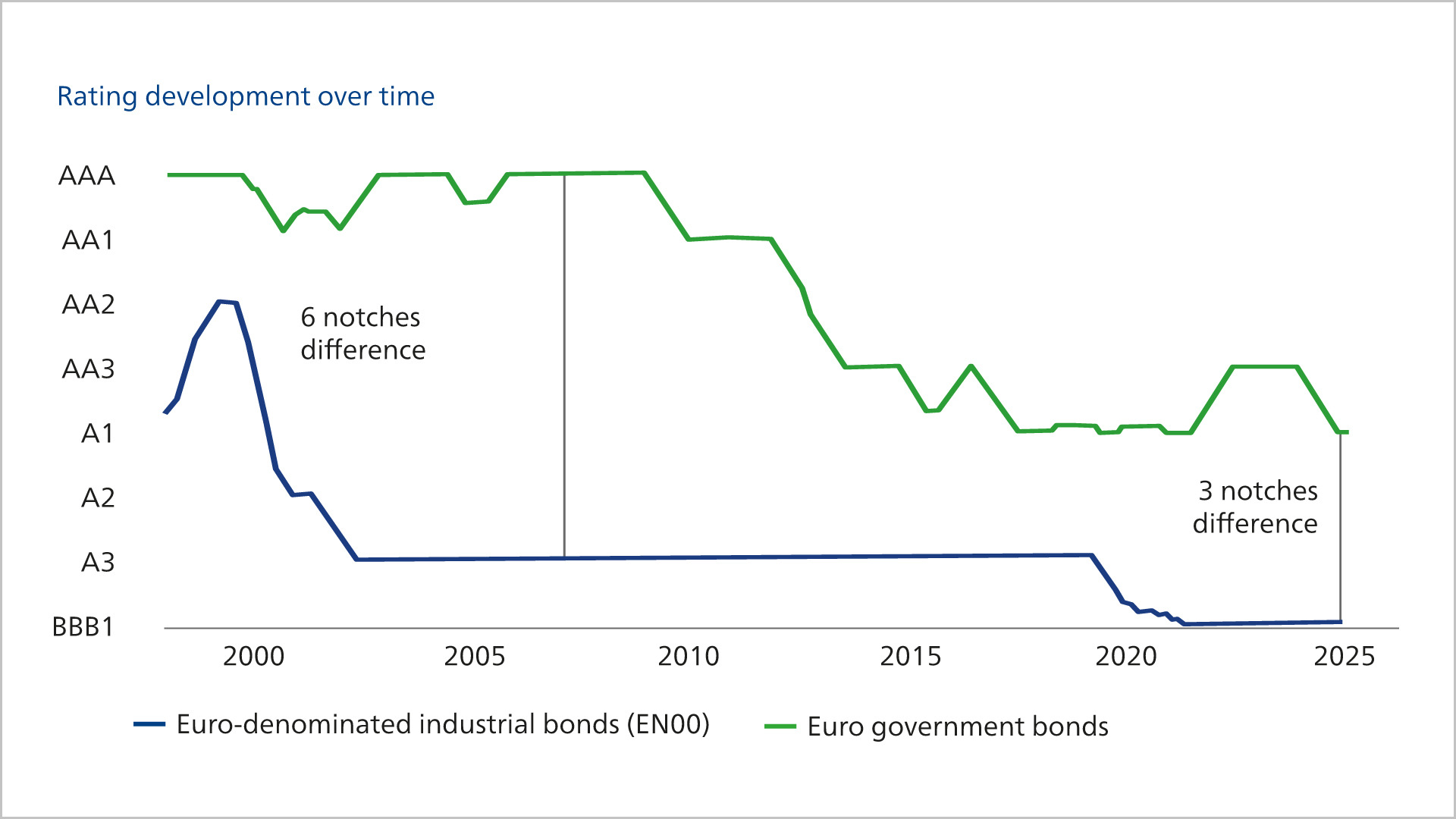

The credit quality is declining.

Source: ICE Indices, Macrobond, Union Investment. As of: December 1, 2025

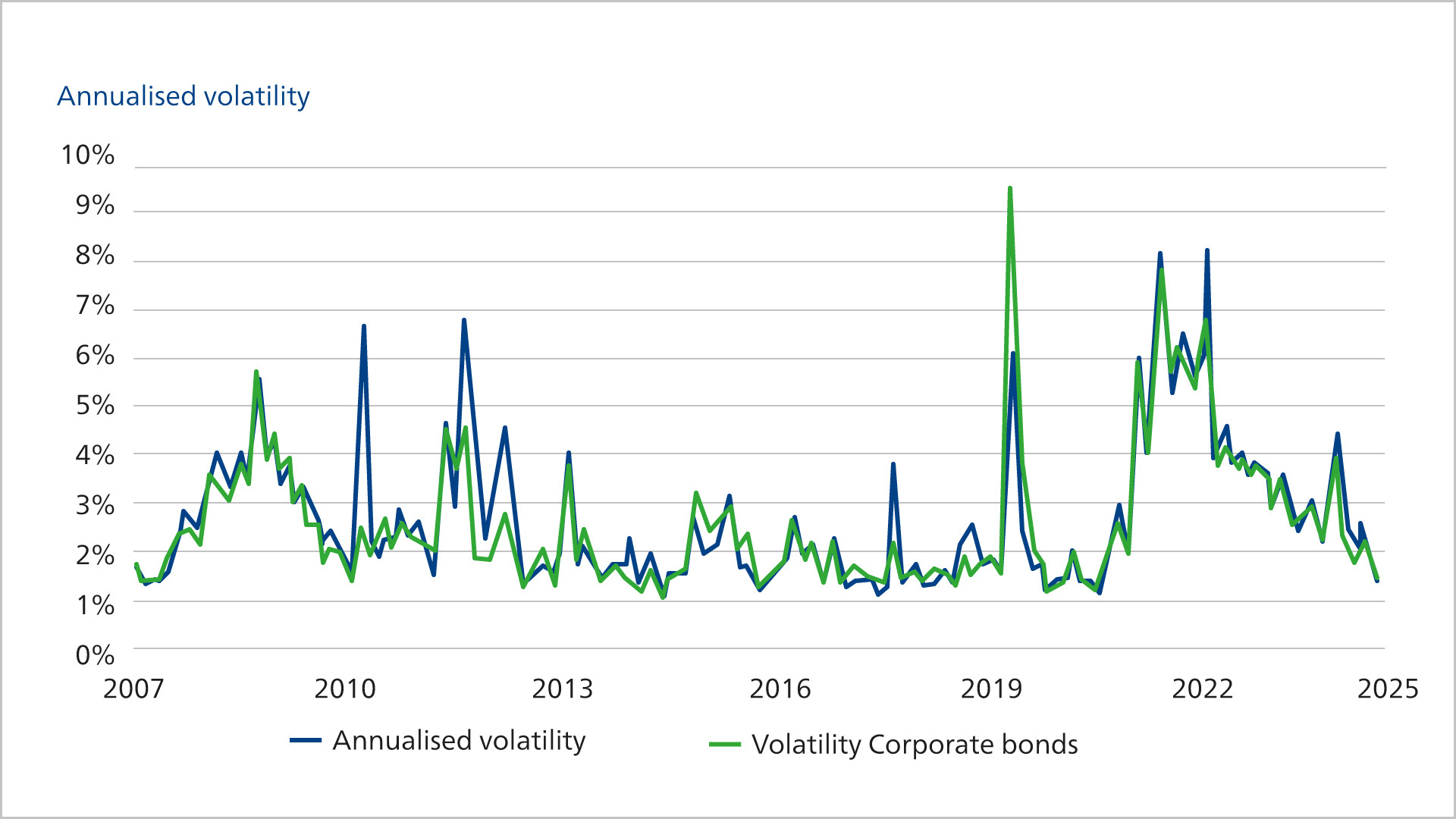

High volatility in government bonds

Source: ICE Indices, Macrobond, Union Investment. As of: December 1, 2025

Keyword Covered Bonds – this bond class requires little risk capital, what else speaks for these securities?

Christian Kopf: Currently, European covered bonds are comparatively attractively priced. When comparing the spread between a senior bond and a covered bond from an institution, it becomes clear that the senior bond offers relatively less pickup for the increased risk. As an addition, we consider covered bonds to be just as suitable as selected emerging market local currency securities, such as those from Brazil or South Africa. For a multi-asset portfolio, inflation-linked bonds may also be worth a look.

And what is there to say about the keyword CLOs?

Christian Kopf: This concerns the securitization of corporate loans. We find this area fundamentally interesting, as the corporate loans being securitized are senior and secured. At the same time, the higher complexity of the securitizations leads to attractive spreads compared to other fixed-income securities. It is also exciting that this year the insurance regulator has decided to significantly reduce the Solvency II capital requirements, in some cases by up to 80 percent, thereby equating the asset class with corresponding alternatives such as corporate bonds or covered bonds. With a variable interest rate and thus a high degree of immunity to interest rate risks, we see this as an exciting investment alternative.

Source: Union Investment, All information, explanations and illustrations are as at 10 Dec 2025, unless otherwise stated