Union Connect: The euro as a global reserve currency: From pretender to heir apparent?

|

The US dollar is the most important global reserve currency, but now the race is being reopened. The euro has a chance to gain global significance – European bond investors would benefit from this. However, a success story is tied to concrete changes.

The dollar's reign shows signs of Instability

"In light of the current changes, the time seems ripe for a greater international role for the euro." This was stated by ECB President Christine Lagarde in May of this year during a speech in Berlin. Is this a realistic assessment? Or, to quote Shakespeare, is "the wish the father of the thought"? The quote from Shakespeare's play "Henry IV" refers to succession to the throne—and this plot fits very well with Lagarde's remark. The undisputed king of currencies has long been, and still is, the US dollar. However, behind the medium- to long-term perspective of this reign now stands a question mark, as we clarified in an analysis last summer (see our position paper "US Dollar: Crisis Currency in Crisis?").

The euro has not been able to benefit

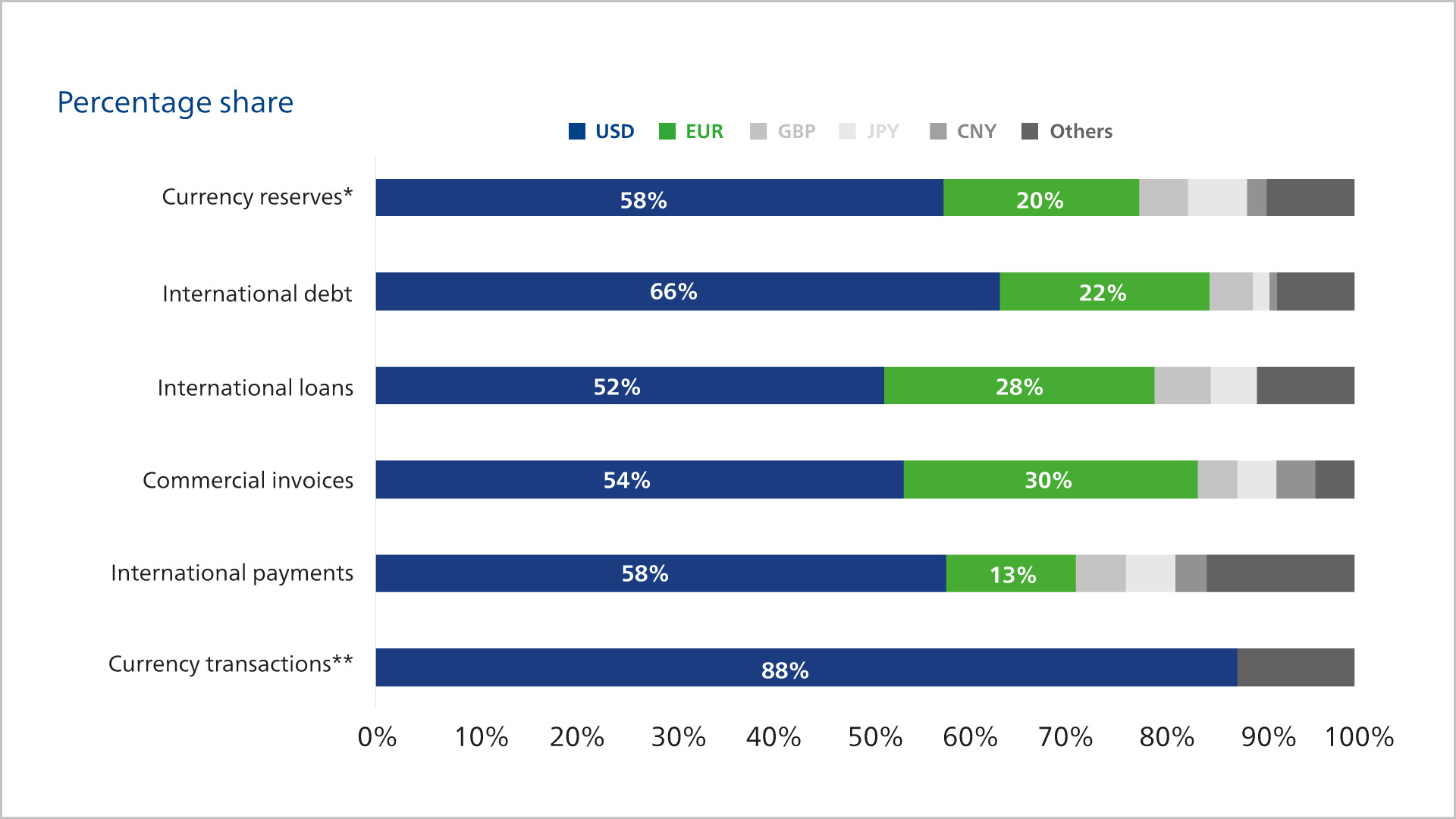

After the dollar, which accounts for 58 percent of global central bank foreign exchange reserves, the euro, with a share of around 20 percent, is the second most important reserve currency in the world. In this respect, the euro is the first candidate to challenge the dollar for the throne.

|

The euro has a share of around 20 percent

the second most important reserve currency in the world.

|

When looking at the recent past, it does not seem that way. Although the share of the dollar in global foreign exchange reserves has fallen by about 15 percentage points since the turn of the millennium, the euro has not really been able to benefit from this. In 2010, it did reach a temporary high with a share of just under 28 percent. However, this was due to an exchange rate of almost 1.50 dollars per euro, not from an active allocation decision by reserve managers. In the meantime, the euro is back at that one-fifth level where it was about 25 years ago. In the last decade, the Chinese renminbi has gained some significance (from 1.0 percent at the end of 2016 to 2.1 percent), as have a number of "smaller" currencies such as the Australian and Canadian dollars (current shares of about 2.0 and 2.6 percent, respectively). At least so far, it seems that the interest of central bank reserve managers has been less focused on switching from one major currency (dollar) to another (euro), but rather on achieving more diversification. When looking at other indicators of a currency's significance, such as cross-border payment transactions or the (nominal) value of internationally issued bonds, the share of the dollar has actually increased in recent years, while that of the euro has decreased.

The question, however, is how much significance the (recent) past has specifically on this topic. The current developments, particularly in the USA, and the medium- to long-term consequences we expect for the dollar suggest that past trends are only conditionally meaningful. What is becoming apparent is a structural break; in other words, the currency race is being partially reopened.

Euro trails as dollar maintains dominance in cross-border transactions

The dollar dominates all types of international financial transactions.

Sources: Atlantic Council, BIS, Boz et al (2022), Brookings, ECB (2023), IMF, Swift, Union Investment. * Share of foreign currency reserves excluding gold. ** USD is involved in 88% of traded currency pairs.

The result is open. It is not certain that the dollar will give up its leading role at all – it may lose some of its edge, but ultimately remains at the forefront. And if not, it is also not set in stone that there will be a new currency king.

The existence of a global reserve currency is primarily supported by economic efficiency – network effects and the complementarity of the various uses of a currency are particularly significant. However, as is well known, the times when everything was subordinated to economic efficiency, as in the heyday of globalization, are temporarily over. In this respect, the new equilibrium among currencies may also appear more multipolar. At least the managers of foreign exchange reserves seem, as mentioned, to be increasingly focusing on diversification.

Deeper European integration as a prerequisite for a stronger euro

As for the euro, it can be summarized as follows: Yes, it has the potential to gain significance, but hardly under the current political and economic conditions. A possible success story of the euro as a reserve currency is tied to concrete changes!

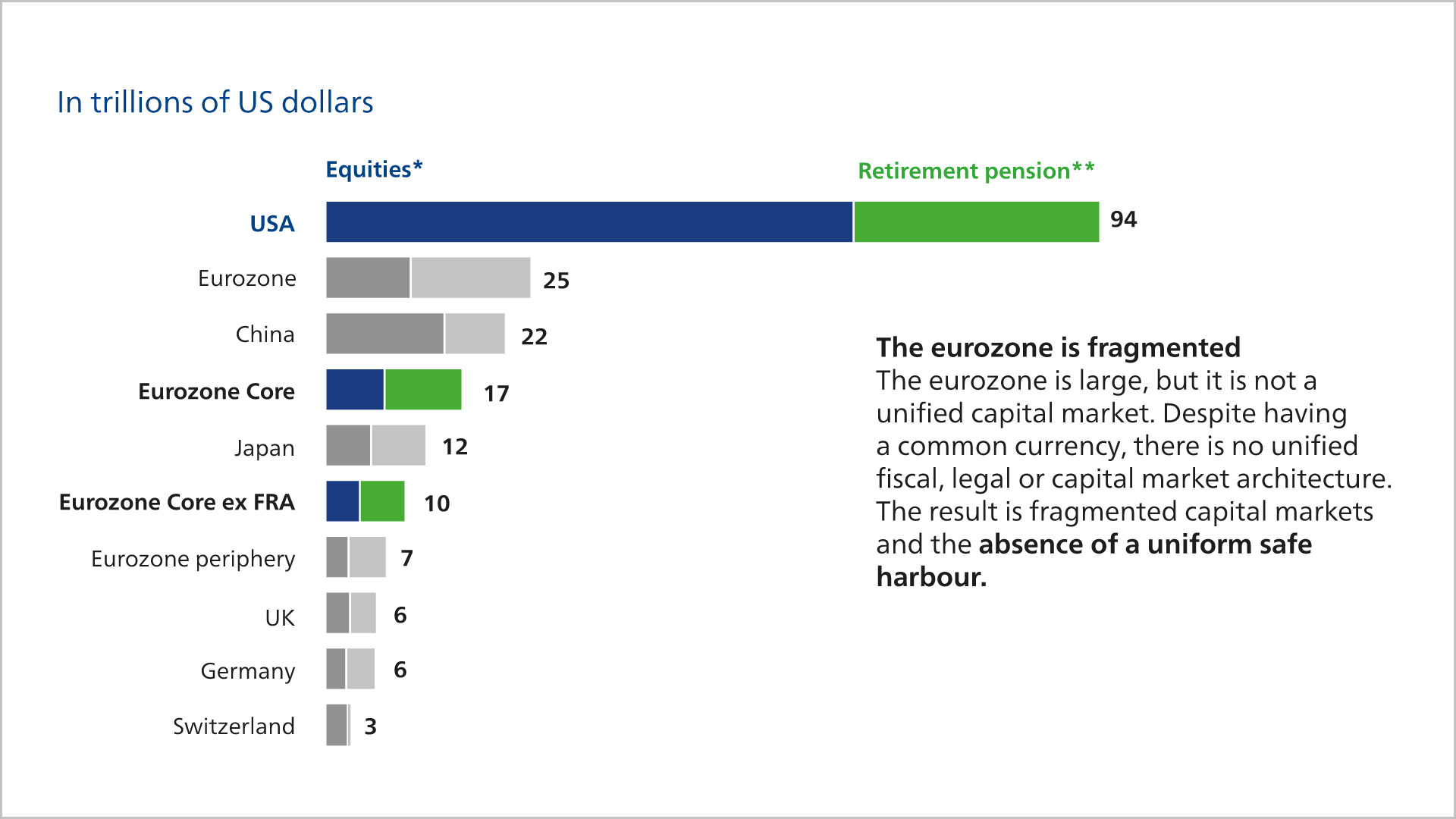

This becomes relatively clear when comparing what distinguishes the USA and what the euro area lacks. At the top of the list is that, from an economic perspective, the economic and monetary union of the euro countries is still incomplete. There is a common currency and monetary policy, as well as a certain legislative competence at the EU level in specific areas. However, compared to the USA, the euro area is still more of a loose association of nation-states, with predominantly its own laws and administrative regulations, different tax and social systems, and divergent fiscal policies. In the political sphere, national interests always take precedence in case of doubt, as can be seen in discussions about potential cross-border corporate mergers. Additionally, there are language barriers and cultural differences that do not exist in the USA, or at least not to this extent.

This becomes relatively clear when comparing what distinguishes the USA and what the euro area lacks. At the top of the list is that, from an economic perspective, the economic and monetary union of the euro countries is still incomplete. There is a common currency and monetary policy, as well as a certain legislative competence at the EU level in specific areas. However, compared to the USA, the euro area is still more of a loose association of nation-states, with predominantly its own laws and administrative regulations, different tax and social systems, and divergent fiscal policies. In the political sphere, national interests always take precedence in case of doubt, as can be seen in discussions about potential cross-border corporate mergers. Additionally, there are language barriers and cultural differences that do not exist in the USA, or at least not to this extent.

Unique USA: No other capital market is as deep and liquid.

Market capitalization of stocks and bond markets

Sources: Bloomberg, Union Investment. As of September 26, 2025. * MSCI All Countries Index, ** Bloomberg Global Aggregate Index.

The euro still has a long way to go – but the direction is right.

One last point about the euro: Historically, leading currencies have been more or less invariably linked to the military strength and geopolitical dominance of the respective country. In this regard, the euro area is (at best) in the second tier, having largely outsourced its defense capability to the USA over decades. Against the backdrop of the threat from Russia and the withdrawal movements of the USA under Donald Trump, there is also a certain trend reversal here, which is expressed, for example, in the "ReArm Europe Plan/Readiness 2030." It can therefore be considered certain that EU countries will increase their military strength in the coming years, but any form of "dominance" is not to be expected.

ECB President Lagarde sees all these challenges, as she later clarified in the aforementioned speech, quite similarly. Her assessment of a possible larger role for the euro is thus quite realistic and not wishful thinking: "The euro," she summarized, "will not automatically gain influence, but will have to earn it." We honestly do not dare to make a concrete prediction about where the euro will stand as a reserve currency in ten years. However, it is likely that its significance will increase. This would be good news for the European capital market and local investors, especially on the bond side. Why is that? If the euro were to become generally more important, it is highly likely that the capital market denominated or settled in euros would also grow larger in parallel – not only absolutely, but also relatively to other currency areas. Ultimately, this would allow euro investors to invest more in their home currency. In the long term, this is usually an advantage, as it is simply cheaper; among other things, it saves the costs of currency hedging. A concrete example is also emerging market bonds that are issued in "hard currency." Currently, these are significantly more often denominated in dollars than in euros. This could shift in the coming years – at least partially – in favor of the euro.

ECB President Lagarde sees all these challenges, as she later clarified in the aforementioned speech, quite similarly. Her assessment of a possible larger role for the euro is thus quite realistic and not wishful thinking: "The euro," she summarized, "will not automatically gain influence, but will have to earn it." We honestly do not dare to make a concrete prediction about where the euro will stand as a reserve currency in ten years. However, it is likely that its significance will increase. This would be good news for the European capital market and local investors, especially on the bond side. Why is that? If the euro were to become generally more important, it is highly likely that the capital market denominated or settled in euros would also grow larger in parallel – not only absolutely, but also relatively to other currency areas. Ultimately, this would allow euro investors to invest more in their home currency. In the long term, this is usually an advantage, as it is simply cheaper; among other things, it saves the costs of currency hedging. A concrete example is also emerging market bonds that are issued in "hard currency." Currently, these are significantly more often denominated in dollars than in euros. This could shift in the coming years – at least partially – in favor of the euro.

Source: Union Investment. All information, explanations and illustrations are as at 3 December 2025, unless otherwise stated